Key Highlights to Navigating Long-Term Care: What You Should Know

December 24, 2021

Key Highlights to Navigating Long-Term Care: What You Should Know

December 24, 2021

Share this post:

Last updated: 02/29/2024

The thought of long-term care (LTC) can feel a bit dismaying with so many questions to answer. What exactly is long-term care? How do you know if you need it? Do you have to “qualify” for it? Having more insight on this topic can help ease some of the confusion or even anxiety around what might be best for you when it comes to assessing LTC as a part of your retirement plan.

WHAT IS LONG-TERM CARE?

With many misconceptions and assumptions about long-term care, it’s important to be clear on what long-term care means. Long-term care consists of a variety of services that include the need for both medical and non-medical assistance—all designed to help an individual meet their physical and medical needs. Generally, long-term care is associated with any personal or medical assistance an individual may need to accomplish their activities of daily living or ADL—think hygiene care, feeding yourself, moving around your home, etc. Typically, long-term care is thought of as care in nursing homes and skilled nursing care. However, a majority of long-term care is provided at home or in adult day health facilities or assisted living facilities.

HOW DO YOU KNOW IF YOU NEED IT?

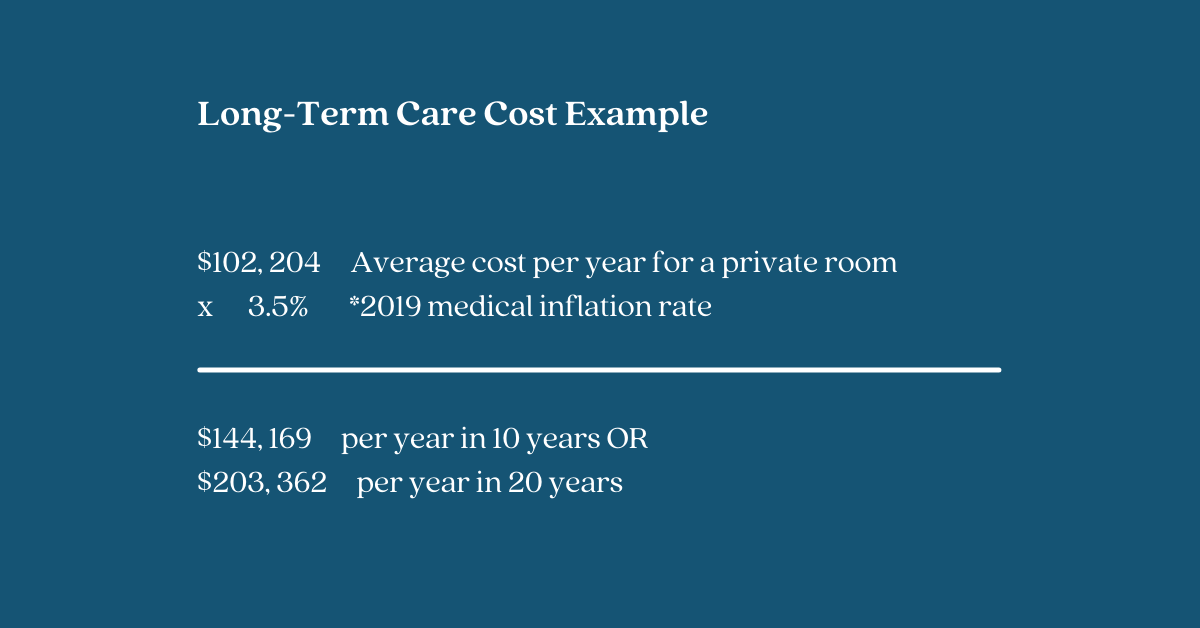

While there may not be a definitive answer and everyone’s situation is unique, planning for LTC within your retirement plan can play a pivotal role in providing an extra level of security. As we know, the cost of living in general tends to rise decade after decade; historical patterns show long-term care is grossly affected annually. To share an example, according to Genworth.com,2 the average annual cost of long-term care for a private room from from now until 2039 will increase by at least 3.5% each decade.

One question to consider when assessing your need for long-term care is, you may never need care, but if you did, how would this affect your family? Here are four important factors to think about if or when a loved one needs care:

- Spouses: The stress of caring for a chronically ill loved one can impact the caregiver’s health as well—physically, mentally, and emotionally.

- Children: Caring for a chronically ill parent tends to affect their career, marriage, children, and family obligations.

- Family dynamics: When informal care is needed, it may not be shared equally amongst adult children. Often, one sibling bears the heavier burden, which can affect the relationship amongst siblings.

- Unnecessary losses: Not all losses can be avoided. However, unnecessary emotional and financial losses can be mitigated when you’re well prepared.

Other things you might consider:

It is difficult to predict how much or what type of long-term care a person might need. Several things increase the risk of needing long-term care.3

- Age. The risk generally increases as people get older.

- Gender. Women are at higher risk than men, primarily because they often live longer.

- Marital status. Single people are more likely than married people to need care from a paid provider.

- Lifestyle. Poor diet and exercise habits can increase a person’s risk.

- Health and family history. These factors also affect risk.

DO YOU QUALIFY FOR LONG-TERM CARE?

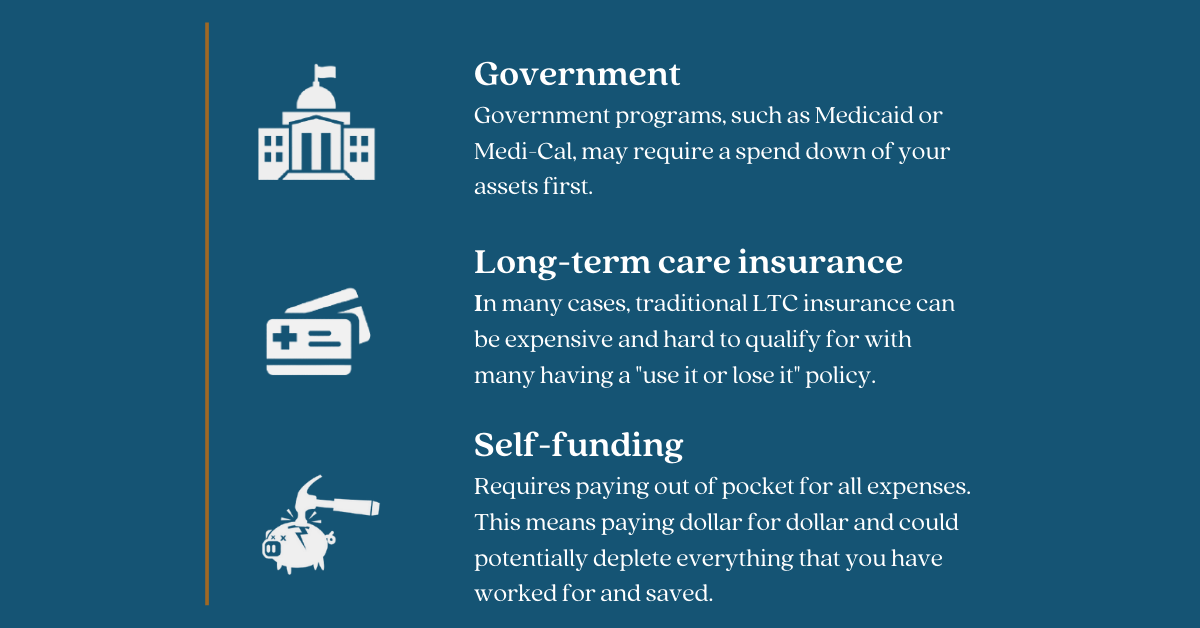

When it comes down to paying for care, it is important to review your financial plan to ensure you are meeting your needs and costs appropriately. Consider this question: If you did need care, how would you pay for it?

While these options certainly have more specifics, including LTC in your overall plan or at least having a conversation with your financial professional can take the guessing out of what might be right for you and your family. Navigating the right options for you, your loved ones, and your future doesn’t have to be done alone.

If you want to learn about more personalized and advanced strategies, schedule a 15-minute call with our team.

Schedule Your Complimentary 15-Minute Call

Want expert retirement and investing advice? Subscribe to our YouTube channel and check out our weekly podcast with The Sandman!

Listen to Protect Your Assets anywhere you get your podcasts:

Standard Disclosure

This blog expresses the author’s views as of the date indicated, are subject to change without notice, and may not be updated. The information contained within is believed to be from reliable sources. However, its accurateness, completeness, and the opinions based thereon by the author are not guaranteed – no responsibility is assumed for omissions or errors. This blog aims to expose you to ideas and financial vehicles that may help you work towards your financial goals. No promises or guarantees are made that you will accomplish such goals. Past performance is no guarantee of future results, and any expected returns or hypothetical projections may not reflect actual future performance or outcomes. All investments involve risk and may lose money. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must evaluate and investigate any investments considered or any investment strategies or recommendations described herein (including the risks and merits thereof), seek professional advice for their particular circumstances, and inform themselves about the tax or other consequences of any investments or services considered. Investment advisory services are offered through Liberty Wealth Management, LLC (“LWM”), DBA Liberty Group, an SEC-registered investment adviser. For additional information on LWM or its investment professionals, please visit www.adviserinfo.sec.gov or contact us directly at 411 30th Street, 2nd Floor, Oakland, CA 94609, T: 510-658-1880, F: 510-658-1886, www.libertygroupllc.com. Registration with the U.S. Securities and Exchange Commission or any state securities authority does not imply a certain level of skill or training.

References

Genworth Financial Inc. (2021, February 12). Cost of Care Survey.

https://www.genworth.com/aging-and-you/finances/cost-of-care.html

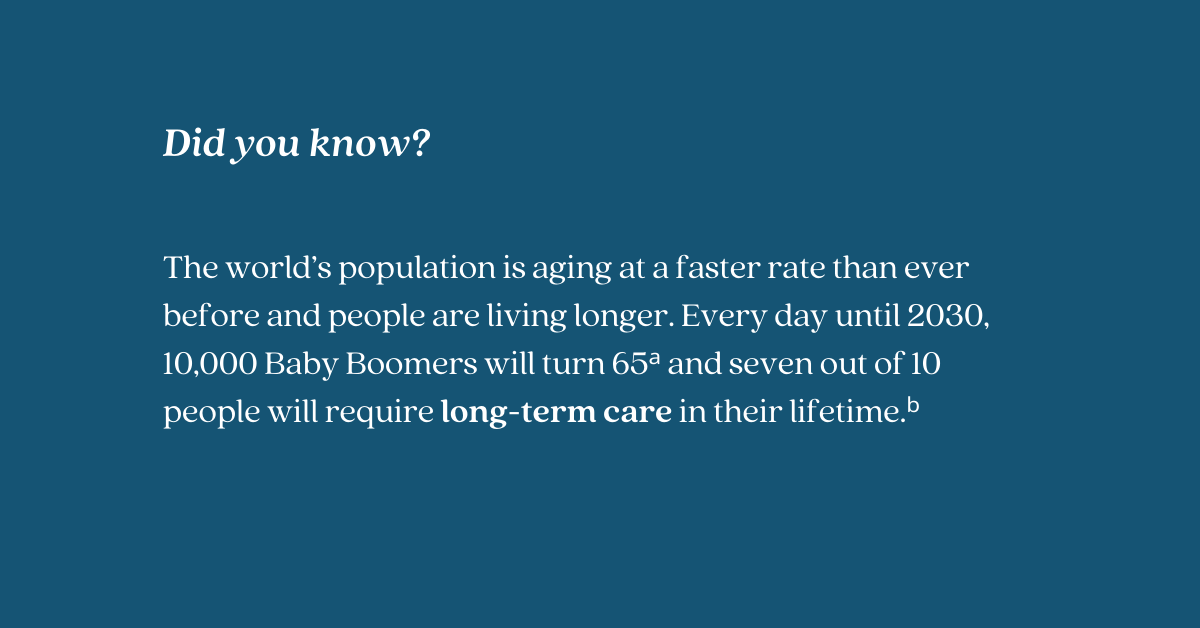

a “2020 Census Will Help Policymakers Prepare for the Incoming Wave of Aging Boomers” https://www.census.gov/library/stories/2019/12/by-2030-all-baby-boomers-will-be-age-65-or-older.html Site accessed 11/04/20.

b 2020 U.S. Department of Health and Human Services. https://acl.gov/ltc/basic-needs/how-much-care-will-you-need Site accessed 04/19/21.

Genworth Financial Inc. (2019, October 16). Genworth 2019 Cost of Care Survey, conducted by CareScout®, June 2019.

https://www.multivu.com/players/English/8625551-8625551-genworth-cost-of-care-survey-2019/

NIH National Institute on Aging (NIA). (2017, May 1). What is Long-Term Care?

https://www.nia.nih.gov/health/what-long-term-care

Insurance Sales Presentation. Lifetime Planning Marketing Inc. CA License #0F17020.