Roth Conversions in 2025: Should You Act Before Tax Rates Change Again?

September 12, 2025

Roth Conversions in 2025: Should You Act Before Tax Rates Change Again?

September 12, 2025

Share this post:

A Roth conversion allows you to move money from a pre-tax retirement account, such as a traditional IRA or 401(k), into a Roth IRA. Taxes are due on the amount converted, but future withdrawals from the Roth account are tax-free under current law.

In 2025, this strategy is gaining more attention. The tax changes introduced by the One Big Beautiful Bill have created a short-term window that could make conversions more appealing for some investors. Tax brackets remain in place, income limits on conversions are still lifted, and a few one-time deductions may apply.

If you are a high earner or approaching retirement, now may be a good time to take a closer look. These rules are set to change after 2025, making this year worth evaluating in your broader tax and retirement strategy.

What the Big Beautiful Bill Changed

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, introduced several tax updates that may affect your Roth conversion decision this year.

1. Income Tax Brackets Remain in Effect

The OBBBA makes the 2017 Tax Cuts and Jobs Act (TCJA) income tax rates permanent. This continuation allows investors to plan conversions under the existing lower tax brackets, which may not be available in future years.

2. Temporary Increase to SALT Deduction Cap

For 2025 only, the state and local tax (SALT) deduction cap increases to $40,000, phasing out at $500,000 of modified adjusted gross income. This change may benefit those who itemize and live in high-tax states.

3. Estate and Gift Tax Exemptions Increased

The federal estate, gift, and generation-skipping transfer tax exemptions are now $15 million per person, indexed for inflation starting in 2026. This provides greater clarity for high-net-worth individuals planning wealth transfers.

4. No Income Limits on Roth Conversions

There are still no income restrictions for Roth conversions. Even high earners can convert pre-tax retirement assets to a Roth IRA, which remains a critical path for building tax-free retirement income.

5. Temporary Deductions and Credits for 2025

Expanded standard deductions, revised charitable giving limits, and updated rules for 529 plans are in effect. For example, this guide to 529 plans outlines how you can use education savings accounts more flexibly in 2025.

These provisions create a different planning landscape for 2025. Whether a Roth conversion is appropriate depends on how these changes interact with your personal goals.

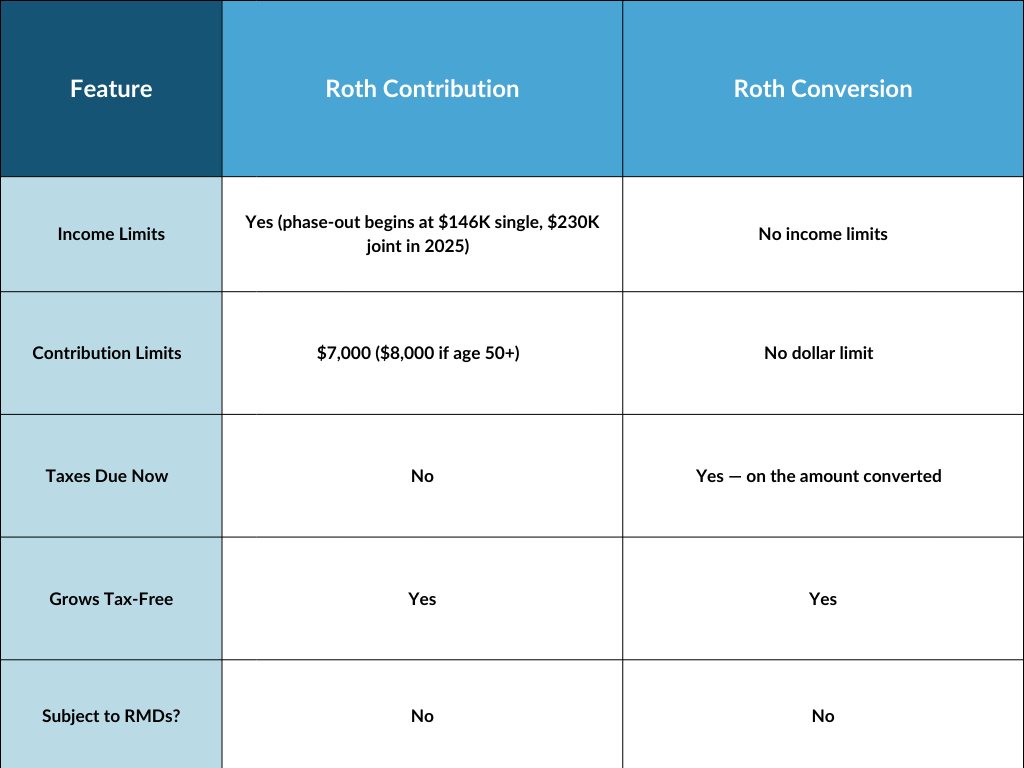

Roth Conversion vs. Roth Contribution: What’s the Difference?

When it comes to building tax-free retirement income, both Roth IRAs and Roth conversions can play a role. But they work differently and the strategy you choose depends on your income level, timing, and broader financial goals.

Here’s a quick comparison:

Roth Contribution vs. Roth Conversion

Explore more on Roth conversion ladders if you’re considering a phased approach over several years.

Why Roth Conversions May Offer More Value for High-Income Households

If your income exceeds the limits for direct Roth IRA contributions, a Roth conversion may be the most effective way to build tax-free retirement income. Conversions also allow larger sums to be moved into a Roth IRA, unrestricted by annual contribution limits.

When Each Strategy May Be Appropriate

A Roth IRA contribution can be suitable for individuals within the income limits who aim to grow their retirement savings tax-free over time.

Roth conversions may offer strategic advantages for those who anticipate being in a higher tax bracket later, want to reduce required minimum distributions in the future, or are focused on estate and legacy planning. With current tax brackets scheduled to remain in place through 2025, some higher earners may view this year as an opportunity to review conversion timing.

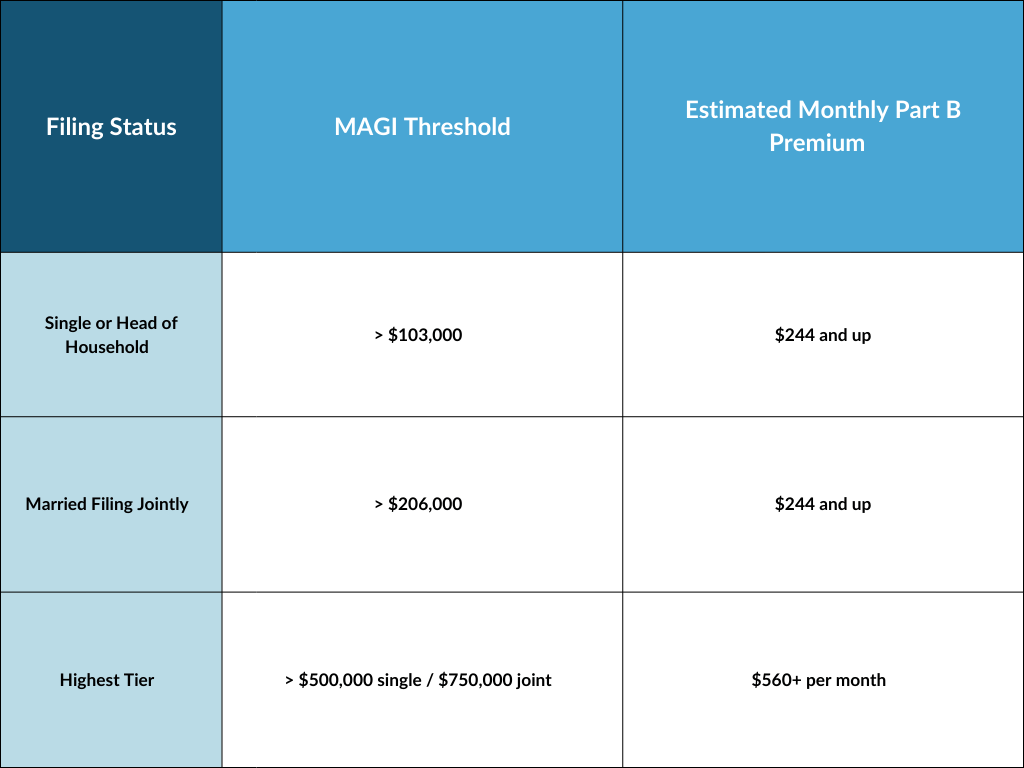

The IRMAA Impact: Medicare Considerations in 2025

Roth conversions increase your modified adjusted gross income in the year they are executed. This added income may affect your overall tax exposure and could influence your future Medicare premiums.

For retirees with higher income, this is especially relevant due to IRMAA, which stands for income-related monthly adjustment amount. IRMAA is a surcharge added to Medicare Part B and Part D premiums when income surpasses specific thresholds.

In 2025, IRMAA tiers begin at the following income levels, based on your 2023 tax return:

Even a single sizable Roth conversion could move you into a higher IRMAA tier for the following year, potentially increasing your monthly Medicare premiums.

This does not mean Roth conversions should be avoided outright, but rather that timing and conversion amounts deserve careful consideration. Using tax projections or consulting with a financial professional may help clarify the tradeoffs.

Strategic Roth Conversion Planning Tips for 2025

If you’re evaluating a Roth conversion in 2025, there are several strategies that may help you approach the opportunity more effectively.

• Convert up to the top of your current tax bracket to avoid triggering a higher marginal rate while taking advantage of available space

• Spread conversions over multiple years to better manage tax impact and Medicare premium exposure

• Use non-retirement assets to pay any resulting tax, helping preserve your retirement balances and avoid penalties if you’re under age 59½

• Factor in estate or legacy plans, as Roth IRAs are not subject to required minimum distributions and may offer strategic benefits when paired with trusts or gifting

• Coordinate with a financial or tax professional to make sure your strategy aligns with your broader retirement goals

Is a Roth Conversion a Good Fit for 2025?

A Roth conversion can be beneficial, but it depends on your overall financial situation. Here are some questions to help guide your decision:

• Will the conversion push you into a higher tax bracket or trigger IRMAA?

• Do you expect to be in a higher tax bracket during retirement?

• Can you pay the tax owed using funds outside your retirement accounts?

• Are you aiming to pass on assets tax-efficiently to heirs?

• Do you need access to the converted funds in the near term?

When It Might Make Sense

• You’re in a relatively low tax bracket this year and expect rates to rise

• You want to reduce future RMDs and retain flexibility

• You’re focused on building a tax-free legacy

When to Proceed Cautiously

• You may need the funds soon and cannot cover the tax burden

• The conversion could increase your Medicare premiums

• You’re already in the highest tax bracket and don’t anticipate changes

Running simulations or talking with a financial professional can help clarify whether now is the right time to convert or if it makes sense to adjust the amount.

Don’t Wait Until It’s Too Late

The 2025 tax law changes introduced under the One Big Beautiful Bill have opened a temporary window that may not last. Acting earlier in the year can give you more control over timing, minimize surprises, and help align your conversion with longer-term planning needs.

To learn more, download Roth Conversions & the Big, Beautiful Bill or connect with our team for a personalized review.

Standard Disclosure

This blog expresses the author’s views as of the date indicated, are subject to change without notice, and may not be updated. The information contained within is believed to be from reliable sources. However, its accurateness, completeness, and the opinions based thereon by the author are not guaranteed – no responsibility is assumed for omissions or errors. This blog aims to expose you to ideas and financial vehicles that may help you work towards your financial goals. No promises or guarantees are made that you will accomplish such goals.

Past performance is no guarantee of future results, and any expected returns or hypothetical projections may not reflect actual future performance or outcomes. All investments involve risk and may lose money. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must evaluate and investigate any investments considered or any investment strategies or recommendations described herein (including the risks and merits thereof), seek professional advice for their particular circumstances, and inform themselves about the tax or other consequences of any investments or services considered.

Investment advisory services are offered through Liberty Wealth Management, LLC (“LWM”), DBA Liberty Group, an SEC-registered investment adviser. For additional information on LWM or its investment professionals, please visit www.adviserinfo.sec.gov or contact us directly at 411 30th Street, 2nd Floor, Oakland, CA 94609, T: 510-658-1880, F: 510-658-1886, www.libertygroupllc.com. Registration with the U.S. Securities and Exchange Commission or any state securities authority does not imply a certain level of skill or training.

References

Watson, Garrett. (July 23, 2025). FAQ: The One Big Beautiful Bill Act Tax Changes. Tax Foundation. https://taxfoundation.org/research/all/federal/one-big-beautiful-bill-act-tax-changes/