Roth Conversions and Medicare Premiums: Understanding the IRMAA Tradeoff

September 19, 2025

Roth Conversions and Medicare Premiums: Understanding the IRMAA Tradeoff

September 19, 2025

Share this post:

Roth conversions have become a popular tax strategy for those looking to reduce future taxable income. By moving funds from a traditional IRA or 401(k) into a Roth IRA, you pay taxes on the converted amount now but benefit from tax-free growth and withdrawals in retirement. Roth IRAs are also exempt from required minimum distributions (RMDs), which may provide more flexibility in later years.

However, one factor that is often overlooked is how a Roth conversion increases your taxable income in the year it occurs. For those on Medicare or approaching enrollment, that additional income could lead to higher premiums through something called the income-related monthly adjustment amount, or IRMAA.

In 2025, understanding this tradeoff is especially important. With a limited window of tax-friendly rules under the Big, Beautiful Bill, more retirees and pre-retirees are considering Roth conversions. Without careful planning, the short-term costs could reduce the long-term benefits.

What Is IRMAA?

IRMAA stands for income-related monthly adjustment amount. It is used to determine how much you will pay for Medicare Part B and Part D premiums. Most people pay the standard Medicare premium. If your modified adjusted gross income (MAGI) exceeds certain thresholds, IRMAA applies and increases your premiums.

Importantly, IRMAA is based on your tax return from two years prior. For example, 2025 Medicare premiums are calculated using your 2023 tax return. That means financial decisions you make this year, such as a Roth conversion, could impact your premiums in the future.

Even a one-time increase in income may move you into a higher IRMAA tier. Understanding how conversions and other financial moves affect your MAGI is essential if you want to manage future healthcare costs.

How Roth Conversions Affect Your Medicare Costs

A Roth conversion increases your MAGI in the year the conversion takes place. Since Medicare uses a two-year lookback, a 2023 conversion could raise your 2025 premiums. Understanding how this works can help you make more informed decisions about the timing and size of a conversion.

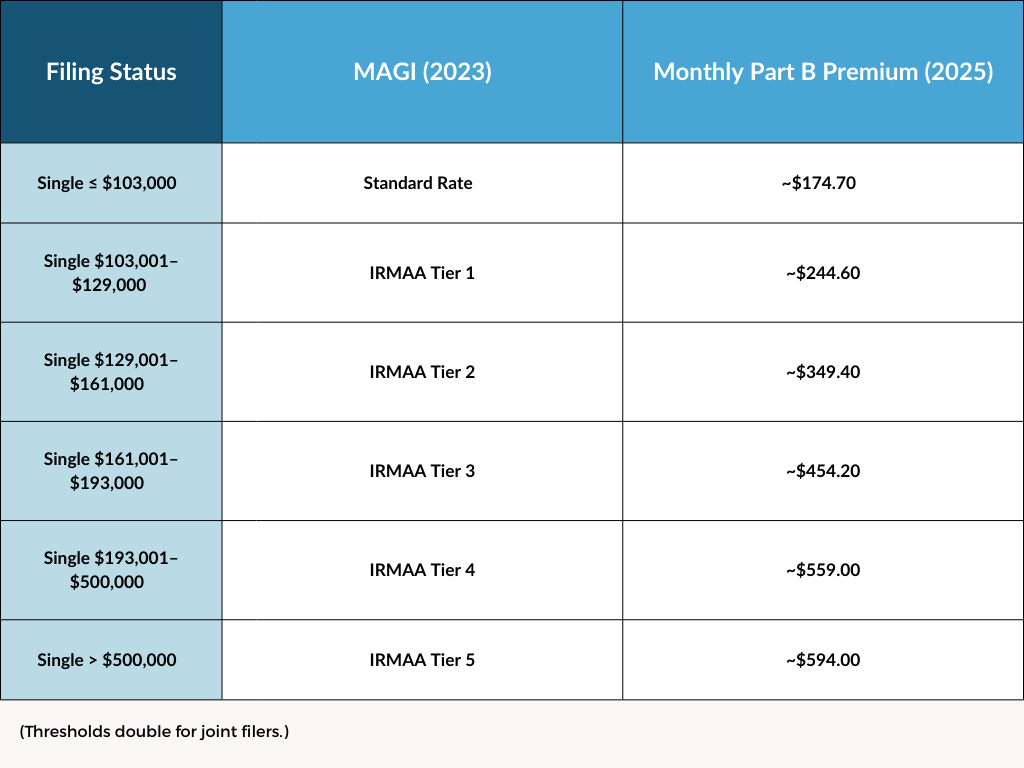

2025 IRMAA Income Thresholds

Here’s how 2023 MAGI (used to determine 2025 premiums) affects what you pay for Medicare Part B:

Example Scenario: The 100,000 Dollar Conversion

Consider a married couple filing jointly with a 2023 MAGI of 230,000 dollars. If they complete a $100,000 Roth conversion, their new MAGI would be 330,000 dollars. That increase could move them from IRMAA Tier 1 to Tier 3.

As a result, each spouse’s Medicare Part B premium may increase by approximately 200 dollars per month. Together, they could pay close to 5,000 dollars more in Medicare premiums for the year. This does not mean Roth conversions should be avoided entirely, but it shows why strategy and timing matter.

Is the Tradeoff Worth It?

Roth conversions can provide long-term benefits such as tax-free growth, elimination of RMDs, and more flexibility for estate planning. For many, they may help reduce future tax burdens and offer more control in retirement.

However, these benefits come with short-term tradeoffs. You will owe income taxes on the converted amount, and your Medicare premiums may increase due to IRMAA.

Whether the tradeoff is worth it depends on several factors:

- How long you plan to keep the funds invested

- Whether you expect to be in a higher tax bracket later

- Your estate planning goals

- How much the IRMAA increase affects your total financial picture

A conversion that is well-timed and sized appropriately may still lead to meaningful long-term benefits, even with a temporary increase in Medicare premiums.

Strategies to Help Manage the IRMAA Impact

If you are considering a Roth conversion in 2025, there are several ways to help manage its effect on IRMAA:

- Convert up to the top of your current tax bracket. Staying just below the next threshold can help you avoid unnecessary increases in premiums.

- Spread conversions over multiple years. Smaller annual conversions may reduce both tax liability and IRMAA exposure.

- Use tax projections or simulations. Modeling different scenarios allows you to see how various conversion amounts could affect future premiums.

- Offset income with other strategies. Qualified charitable distributions (QCDs) and tax-loss harvesting may help reduce your MAGI in the year of conversion.

These techniques can help you balance long-term tax efficiency with near-term Medicare considerations.

When to Avoid or Delay a Conversion

There are situations where delaying a conversion may be more beneficial than doing it right away:

- You are retiring soon and expect lower income in future years. Waiting could let you convert at a lower tax cost and reduce IRMAA exposure.

- You are already in the highest IRMAA tier. A conversion might not increase your premiums further, but you will still pay the tax on the converted amount.

- You have a short time horizon or limited interest in legacy planning. If your goal is to use your retirement savings yourself, the long-term Roth benefits may be less significant.

Delaying a conversion or scaling back the amount could offer greater control over both taxes and premiums.

Plan With the Full Picture in Mind

Roth conversions can be a valuable part of a long-term tax strategy. But they need to be evaluated in the context of your total financial picture, including healthcare costs and timing. IRMAA is not necessarily a reason to avoid conversions. It is simply one piece of the planning process that should not be overlooked.

Before making a decision, talk with a financial professional. An advisor can help you consider the pros and cons, evaluate timing, and coordinate your conversion with other aspects of your financial plan.

Download our free guide, “Roth Conversions and the Big, Beautiful Bill: Your 2025 Guide to Strategic Tax Planning”, or schedule a complimentary review to explore what makes sense for your goals.

Standard Disclosure

This blog expresses the author’s views as of the date indicated, are subject to change without notice, and may not be updated. The information contained within is believed to be from reliable sources. However, its accurateness, completeness, and the opinions based thereon by the author are not guaranteed – no responsibility is assumed for omissions or errors. This blog aims to expose you to ideas and financial vehicles that may help you work towards your financial goals. No promises or guarantees are made that you will accomplish such goals.

Past performance is no guarantee of future results, and any expected returns or hypothetical projections may not reflect actual future performance or outcomes. All investments involve risk and may lose money. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must evaluate and investigate any investments considered or any investment strategies or recommendations described herein (including the risks and merits thereof), seek professional advice for their particular circumstances, and inform themselves about the tax or other consequences of any investments or services considered.

Investment advisory services are offered through Liberty Wealth Management, LLC (“LWM”), DBA Liberty Group, an SEC-registered investment adviser. For additional information on LWM or its investment professionals, please visit www.adviserinfo.sec.gov or contact us directly at 411 30th Street, 2nd Floor, Oakland, CA 94609, T: 510-658-1880, F: 510-658-1886, www.libertygroupllc.com. Registration with the U.S. Securities and Exchange Commission or any state securities authority does not imply a certain level of skill or training.