How to Survive a Recession: 7 Steps to Take Now to Prepare for an Economic Downturn

October 21, 2022

How to Survive a Recession: 7 Steps to Take Now to Prepare for an Economic Downturn

October 21, 2022

Share this post:

Date Last Updated: October 10, 2024

Economic downturns can be nerve-wracking and challenging to know how to survive—and the word recession is a big scary word for many, especially those who experienced the recessions in the early 2000s and 2009.

A recession is a substantial decline in general economic activity, measured by a variety of methods (you can read more about recessions here). Official recessions can only be declared by the National Bureau of Economic Research after they occur, but that doesn’t stop many financial experts and the media from speculating in the meantime—from The New York Times: U.S. Economy Shows Another Decline, Fanning Recessions Fears; from CNBC: Danger ahead: The U.S. economy has yet to face its biggest recession challenge. With headlines like these, what can you do to tame your fears and successfully survive an economic downturn?

Keep in mind that preparing for an economic downturn is a proactive measure—something that you should start doing early and regularly. You can change your financial habits to better insulate your money and mitigate risk from a recession.

Seven Tips to Make Your Finances More Resilient During Economic Downturns

1. Manage your emotions and avoid panic selling

It can be tempting to pull your money out of the market when the economy is trending downward, but this is often historically one of the worst times to sell. The stock price has already dropped, so you’re selling at a discount, thus ensuring losses. Many financial professionals and market experts will recommend that you hold your investments instead. According to The Motley Fool, “You don’t technically lose any money unless you sell, so by holding onto your stocks until the market eventually recovers, you can ride out the storm.”

Investing is a long-term game, something that can be hard to remember when your country is amid economic turmoil. Understanding what’s driving the market drops and avoiding constant checking of the headlines and your accounts can help you keep your cool, too. Remember: Recessions don’t last forever and are often followed by periods of economic growth and prosperity. NBER data tracking recessions between 1945–2009 found that the average recession lasted 11 months. According to Putnam, “History has shown that markets bounce back, and that staying invested through volatile episodes lets you benefit from a rebound.”

If you feel you absolutely must sell, just remember it’s near impossible to time the market consistently. How do you know when to get back in? Before making any moves, take a bit of time, talk to a neutral third party—or even better—a financial professional, and make the decision with a clear head.

2. Review your asset allocation

An essential part of protecting any investment, including your retirement accounts, is to be sure your allocations match your investing horizon, financial goals, and risk tolerance. In general, the closer you are to retirement, the more conservative your portfolio might look because you have fewer years to recover from losses and will begin withdrawing from your accounts in your nearing—or current—retirement. If a recession is looming, some financial professionals will advise those at or close to retirement to shift a little money out of stocks and into cash investments—but this isn’t always the best-case scenario.

Avoiding highly volatile growth stocks can limit your return potential if the market shifts in their favor but keep your investments safer during a recession. Less volatile/risky stocks from high-quality, stable companies can pad your investments when the economy is tough.

3. Diversify your investments

According to Investopedia, “If you don’t have all of your money in one place, your paper losses should be mitigated, making it less difficult emotionally to ride out the dips in the market. If you own a home and have a savings account, you already have a start: You have some money in real estate and some money in cash. In particular, try to build a portfolio of investment pairs that aren’t strongly correlated, meaning that when one is up, the other is down, and vice versa (like stocks and bonds).”

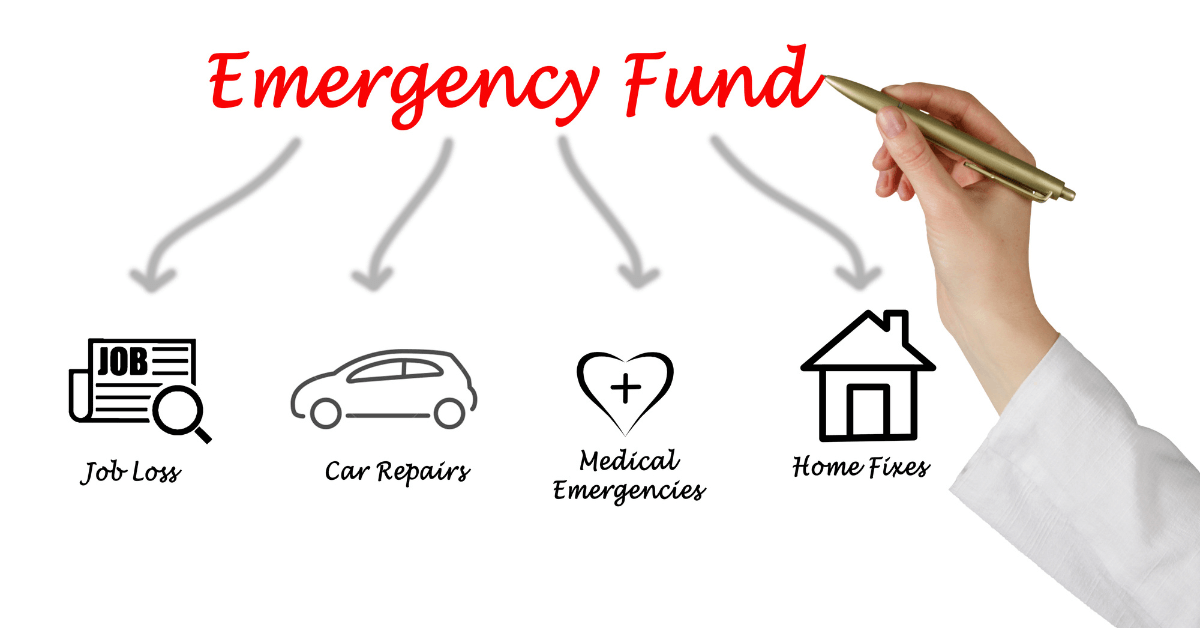

4. Establish and frequently contribute to an emergency fund

You need a safety net no matter what, but this comes into play especially when the economy is struggling and layoffs, job loss, and pay/hour cuts are more commonplace. Common advice is to have enough money in an emergency fund to pay for 3–6 months of expenses—but don’t stop there if you have the means to put more into savings. If saving money is difficult for you or not within your budget, just remember any amount you can save will be helpful. To increase your odds of success, set up a specific account to hold your emergency funds and automatically divert some of your paycheck to this account.

5. Pay down your debt and refinance variable interest rates into fixed rates

We recognize this may not be possible if a recession has already hit. In this respect, we’re including this as more of a proactive measure you can take before an economic downturn but can be very important to reducing your anxiety and freeing up some additional money in case a recession does occur. Start with your high interest debt, like credit cards, and work your way through the rest when possible.

When the Fed raises interest rates, variable interest debts are usually directly impacted, too, making borrowing money and carrying debt from month to month more expensive. If you can refinance these debts into fixed rate loans, you could save yourself money.

6. Make changes to your spending habits

An important internal conversation to have when the economy is on a downward spiral is which of your current spending habits will no longer serve you when money is tighter. What discretionary expenses can you trim? Think travel costs, food costs like eating out or getting a daily coffee, and automatic payments on apps or streaming services. Now, think of what expenses you may consider “essential” but might not be? Think a gym membership, cable TV, or lawncare expenses. Lastly, how can you change your habits to be more conscious of your spending? Most of us don’t think twice about swiping our card for everything or quickly clicking ‘Buy Now’ on Amazon—but these can be mindless costs that you’re not consciously thinking through before purchasing. Now might not be the time for a big purchase, either. Before purchasing a car, booking that dream vacation, or starting that kitchen remodel, look at your overall financial picture and determine if it’s really the right time to spend that money.

Creating a monthly budget can also help you plan your spending in an economic downturn. Bankrate recommends to “Write down every financial firm you regularly work with and whom you regularly pay a bill to. See how much cash you have available right now, whether in a checking or savings account. Find out the categories where you spend money most. It’s always a good idea to go through your monthly expenses and identify which items are discretionary — services or items you can live without — and which items are a necessity. Creating a monthly budget is even more important to ensure you’re living within your means and not overspending.”

7. Look for a side gig

Yes, this tip isn’t for everyone! If you have a hidden talent, interest, or, dare we say, even a passion that you could turn into a side hustle, there just might be an avenue out there to earn extra income. You could also look at a part-time gig in an industry you’re interested in to earn additional money.

Unfortunately, there’s no escaping the ups and downs of the stock market or economy—it’s a fact of living in any society. But there are ways to mitigate your risk and losses and hopefully come out the other side…maybe even better off than you were before. Bankrate states, “Taking steps to prepare your wallet for a downturn when times are good can help take away some of the stress and worry surrounding recessions.

If you want to learn about more personalized and advanced wealth management strategies, schedule a 15-minute call with the Liberty Group team.

Schedule Your Complimentary 15-Minute Call

Want expert retirement and investing advice? Subscribe to our YouTube channel and check out our weekly podcast with The Sandman!

Listen to Protect Your Assets anywhere you get your podcasts:

Standard Disclosure

This blog expresses the author’s views as of the date indicated, are subject to change without notice, and may not be updated. The information contained within is believed to be from reliable sources. However, its accurateness, completeness, and the opinions based thereon by the author are not guaranteed – no responsibility is assumed for omissions or errors. This blog aims to expose you to ideas and financial vehicles that may help you work towards your financial goals. No promises or guarantees are made that you will accomplish such goals.

Past performance is no guarantee of future results, and any expected returns or hypothetical projections may not reflect actual future performance or outcomes. All investments involve risk and may lose money. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must evaluate and investigate any investments considered or any investment strategies or recommendations described herein (including the risks and merits thereof), seek professional advice for their particular circumstances, and inform themselves about the tax or other consequences of any investments or services considered.

Investment advisory services are offered through Liberty Wealth Management, LLC (“LWM”), DBA Liberty Group, an SEC-registered investment adviser. For additional information on LWM or its investment professionals, please visit www.adviserinfo.sec.gov or contact us directly at 411 30th Street, 2nd Floor, Oakland, CA 94609, T: 510-658-1880, F: 510-658-1886, www.libertygroupllc.com. Registration with the U.S. Securities and Exchange Commission or any state securities authority does not imply a certain level of skill or training.

References

Allianz. (July 25, 2022). The Most Worry in Years: Americans Are Increasingly Anxious About a Recession As Inflation Cuts into Spending Power. https://www.allianzlife.com/about/newsroom/2022-press-releases/americans-are-increasingly-anxious-about-a-recession-as-inflation-cuts-into-spending-power

Brockman, Katie. (July 15, 2022). 3 Ways to Help Your Investments Survive a Recession. The Motley Fool. https://www.fool.com/investing/2022/07/15/3-ways-to-help-your-investments-survive-recession/

Federal Reserve. (May 2022). Economic Well-Being of U.S. Households in 2021. https://www.federalreserve.gov/publications/files/2021-report-economic-well-being-us-households-202205.pdf

Foster, Sarah. (August 18, 2022). 9 ways to prepare your finances for a recession. Bankrate. https://www.bankrate.com/banking/federal-reserve/how-to-prepare-for-a-recession/

Fox, Michelle. (July 6, 2022). 74% of consumers are concerned about a recession: 5 steps you can take now to prepare. CNBC. https://www.cnbc.com/2022/07/05/what-you-can-do-to-prepare-your-finances-for-a-recession.html

Harris, Diane. (October 4, 2019). How to Survive a Recession: 12 Steps You Should Take Now to Protect Your Money. Newsweek. https://www.newsweek.com/12-steps-you-should-take-protect-your-money-prepare-next-recession-1463199

Investopedia. (June 24, 2022). 7 Ways to Recession-Proof Your Life. https://www.investopedia.com/articles/pf/08/recession-proof-your-life.asp

Kerr, Emma. (July 7, 2022). 5 Ways to Survive an Economic Downturn. U.S. News. https://money.usnews.com/money/personal-finance/spending/articles/ways-to-survive-an-economic-downturn

Putnam Investments. (February 2022). Markets recover from crises. https://www.putnam.com/literature/pdf/II511.pdf

Singletary, Michelle. (June 15, 2022). Seven ways you can financially prepare for a recession. Washington Post. https://www.washingtonpost.com/business/2022/06/15/7-tips-on-how-to-survive-a-recession/