Inflation: What It Is and Why You Should Care

July 7, 2021

Inflation: What It Is and Why You Should Care

July 7, 2021

Share this post:

Last Updated: February 14, 2024

Have you ever heard your grandparent say, “I remember when a gallon of milk cost 30 cents!”? Shoot, you may even have examples from your lifetime! I remember when a gallon of gas was a little over a dollar—and I’m a millennial. There’s one big reason for these stories of “better times” when things cost much less: inflation.

What Is Inflation?

Put simply: Inflation is when the price of goods increases—essentially, the prices for almost everything going up at the same time—thus reducing the purchasing power (or value) of your money and increasing the cost of living. Inflation can be very obvious, like when the prices of goods jump significantly and quickly, or less apparent, like with inflation over the long term. Long-term inflation is a gradual and steady increase of goods over time, like the story above.

How Inflation Is Measured and Managed

The most commonly used metric to measure inflation is the consumer price index, or CPI. The U.S. Bureau of Labor Statistics surveys 23,000 businesses and records the price of 80,000 items each month, monitoring the average price change of eight categories of goods and services: recreation, transportation, apparel, medical care, housing, food, education and communication, and other goods and services. The Fed removes energy and food prices from the core inflation rate, as these prices change frequently and are too volatile to be factored into the consideration.

Another metric that measures inflation is called the personal consumption expenditures price index, or PCE. The U.S. Bureau of Economic Analysis calculates PCE from a different and more extensive group of goods than the CPI metric. The wholesale price index, or WPI, and producer price index, or PPI, are two additional measures of inflation. The WPI measures the price of goods leading up to retail distribution—at the wholesale level. This is not commonly used in the U.S. to measure inflation; instead, we use the PPI, which measures price changes from the seller’s standpoint, in contrast to the CPI, which measures price changes at the consumer level.

To measure inflation, calculate the percent change in CPI over a certain time period. There are also a variety of inflation calculators accessible online.

Central banks and the Federal Reserve implement policies to avoid inflation—and deflation, taking measures to manage the money supply and credit. The U.S. Federal Reserve targets an annual inflation rate of 2%. The Fed enacts monetary policies like price stability, high employment levels, and moderate interest rates—even taking interest rates to zero in extreme economic conditions, like the 2008 financial crisis.

Causes of Inflation

This is a highly debated topic, but it’s generally accepted that supply and demand and/or rising costs of production, labor, or materials are the main causes of inflation. Another third cause, an increase in the money supply, is sometimes cited as a cause of inflation (though, there are examples of the government printing more money with no significant effects on inflation), but the Federal Reserve considers this a type of demand-pull inflation, not a standalone cause.

Inflation Types

Inflation types are characterized either by the cause or rate of increase.

- Cost-push: when the cost to produce goods and services increases, thus pushing prices higher. The rising prices of raw materials or labor can cause this.

- Demand-pull: when the demand for goods and services outpaces production.

- Creeping: slow inflation, when prices rise less than 3% a year

- Walking (trotting): moderate price increases, but the inflation rate is still in the single digits

- Running (galloping): significant price increases when the inflation rate is in double digits (10% or greater a year)

- Hyperinflation: exceptional, out-of-control inflation (over 1000% a year). The most famous example (though certainly not the worst case) of this happened in Germany in the aftermath of World War I. After the war, Germany was forced to pay reparations for the damage caused by the war but, as a condition, couldn’t pay them in its own currency. This led the German government to print more money to buy foreign currency to pay these reparations, which astronomically devalued the German mark, leading to hyperinflation (and significantly contributing to the ominous chain of events that led to Hitler taking power and World War II).

- Stagflation: high inflation, even in the midst of an economic downturn or recession

- Asset inflation: when the prices of assets, like gold and real estate, rise

Alternatives to Inflation

- Deflation: inflation’s opposite, meaning a negative inflation rate or price drop of goods and services. An example of deflation is the Great Depression—the cost of goods fell because people couldn’t afford to buy them due to unemployment, the stock market crash, and other contributing factors.

- Disinflation: a falling inflation rate or slowing of price increases of goods and services.

- Reflation: a way the government curbs inflation by purposely stimulating the economy by increasing the money supply or government spending. Good examples of this are the economic stimulus payments as a result of the Covid-19 pandemic and, according to some, the 2008 bank bailouts under the Emergency Economic Stabilization Act of 2008. Lowering interest rates can also help jumpstart the economy and curb inflation.

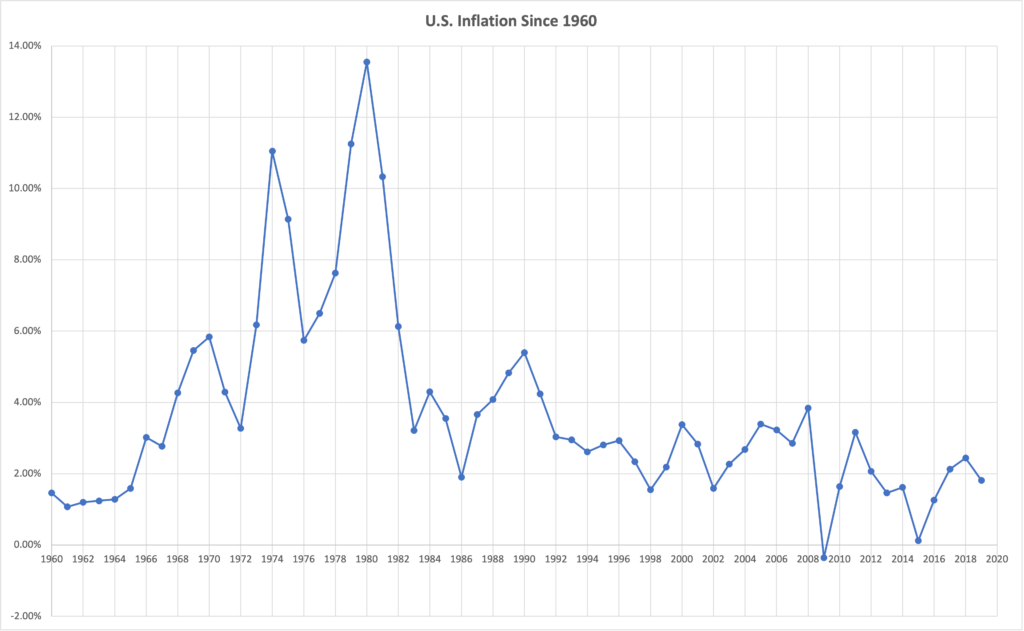

Inflation in the U.S.

From 1960 to 2019, the U.S. inflation rate averaged 3.72% annually. From 2000 to 2019, the inflation rate averaged 2.17% annually. The prices of different goods and services can rise at different rates; healthcare and college tuition typically outpace the annual average inflation rate. For example, tuition generally increases at more than double the general inflation rate, averaging about 8% a year and doubling the cost of tuition—staggeringly—every nine years, according to finaid.org. According to cms.gov, the spend on healthcare is expected to increase annually an average of 5.8% between 2019–2028.

Source: https://www.macrotrends.net/countries/USA/united-states/inflation-rate-cpi

Is Inflation Bad?

Inflation is certainly a dirty word to most, but should it be? High inflation is generally bad for the economy, but too little inflation can also be a negative. Moderate inflation (about 2% a year, the Fed’s goal) is important to help drive consumer spending and consumption—both key factors for economic growth. Slow price increases encourage people to keep spending by preventing consumers from waiting for lower prices to purchase, which helps keep businesses in the black and keeps supply and demand manageable. Inflation can also prevent deflation, which can be incredibly damaging to the economy.

When inflation is on the rise, the loss of purchasing power harms those who hold much of their wealth in cash because their money is worth less. It can also have a detrimental effect on lower-wage workers, as their wages don’t keep pace with rising costs, though it certainly impacts businesses, workers, and consumers at all levels. Borrowers can benefit because they pay back their loans with cash that’s worth less than the value at which they acquired the loan. High inflation can encourage spending because consumers want to purchase goods and services before the prices rise—which can sometimes happen daily. This benefits sellers but is disadvantageous for buyers.

Hedging Against Inflation

A diversified portfolio is the best protection against inflation; carrying all of your assets in cash (or any one other class) is a dangerous financial plan. The stock market traditionally delivers returns greater than the inflation rate, and there are inflation-protected investments, like treasury inflation protected securities, that are invested to keep pace with inflation. A financial professional can help you select and invest in the right assets and securities to diversify your portfolio and incorporate inflation protection, if desired. If inflation is on your mind, don’t fear: There may be options that can help you protect the value of your money. Investing your money appropriately is one of main ways to keep up with inflation.

Why Inflation Matters

Inflation’s impact can be felt at almost all levels of the economy and society and lowers the purchasing power of your money. It affects everyone’s standard of living, savings, spending, and job. Understanding what inflation is and how you can protect yourself is crucial to continuing to live the way you want—even in the midst of rising prices and lower purchasing power.

If you want to learn about more personalized and advanced strategies, click HERE to schedule a 15-min call with our team.

Want expert retirement and investing advice? Subscribe to our YouTube channel and check out our weekly podcast with The Sandman!

Listen to Protect Your Assets anywhere you get your podcasts:

Standard Disclosure

This blog expresses the author’s views as of the date indicated, are subject to change without notice, and may not be updated. The information contained within is believed to be from reliable sources. However, its accurateness, completeness, and the opinions based thereon by the author are not guaranteed – no responsibility is assumed for omissions or errors. This blog aims to expose you to ideas and financial vehicles that may help you work towards your financial goals. No promises or guarantees are made that you will accomplish such goals. Past performance is no guarantee of future results, and any expected returns or hypothetical projections may not reflect actual future performance or outcomes. All investments involve risk and may lose money. Nothing in this document should be construed as investment, tax, financial, accounting, or legal advice. Each prospective investor must evaluate and investigate any investments considered or any investment strategies or recommendations described herein (including the risks and merits thereof), seek professional advice for their particular circumstances, and inform themselves about the tax or other consequences of any investments or services considered. Investment advisory services are offered through Liberty Wealth Management, LLC (“LWM”), DBA Liberty Group, an SEC-registered investment adviser. For additional information on LWM or its investment professionals, please visit www.adviserinfo.sec.gov or contact us directly at 411 30th Street, 2nd Floor, Oakland, CA 94609, T: 510-658-1880, F: 510-658-1886, www.libertygroupllc.com. Registration with the U.S. Securities and Exchange Commission or any state securities authority does not imply a certain level of skill or training.